IAS 7 Statement of cash flows

Tax Guide: IAS 7 Statement of cash flows

IAS 7 prescribes how to present information in a statement of cash flows about how an entity’s cash and cash equivalents changed during the period.

An entity should present its cash flows in the manner most appropriate to its business.

OBJECTIVE

To provide users of financial statements with a basis to assess:

- the ability of the entity to generate cash and cash equivalents, and

- the needs of the entity to utilise those cash and cash equivalents.

Users of financial statements also consider the entity’s cash generating ability and cash needs to evaluate its liquidity position in order to take economic decisions as the entity needs cash to carry on its operations, for payment of its liabilities and distributions of returns to its investors.

CASH AND CASH EQUIVALENTS

Cash and cash equivalents consists of

- Cash

cash on hand and demand deposits.

- Cash equivalents

short-term, highly liquid investments (generally less than three months from date of acquisition) that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. This may include bank overdrafts.

- Cash equivalents

Classification of cash flows

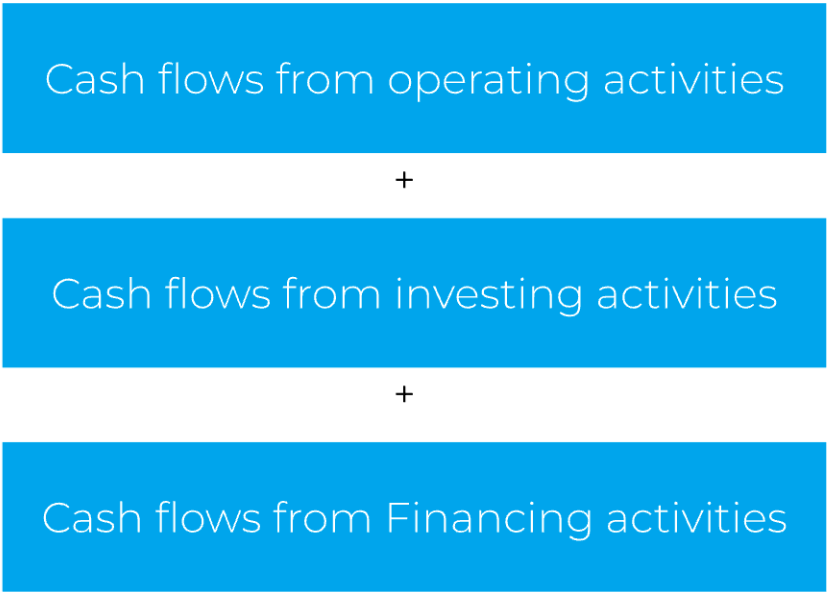

Cash flows during the period are classified as:

- Operating activities

are the principal revenue-producing activities of the entity and other activities that are not investing or financing activities. An entity reports cash flows from operating activities using either the:

- Direct method

major classes of gross cash receipts and gross cash payments (i.e., each category of inflow and outflow) are disclosed; or - Indirect method

profit or loss is adjusted for non-cash transactions, working capital changes and items of income or expenditure associated with investing or financing cash flows.

- Direct method

- Investing activities

are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. This includes the aggregate cash flows arising from obtaining and losing control of subsidiaries or other businesses. These cashflows should be reported net of cash and cash equivalents acquired or disposed of. - Financing activities

activities that result in changes in the size and composition of the contributed equity and borrowings of the entity Cash payments made by lessees for the reduction of lease liabilities are financing activities.

OTHER CLASSIFICATION CONSIDERATIONs

Cash flows must be reported gross. Offsetting is only permitted in very limited cases and additional disclosures are required.

Specific guidance exists around some types of cash flows where classification elections are available. Cash flows should be classified consistently from period to period.

- Income taxes

income tax payments are usually classified as operating activities, although in specific circumstances they can be classified within financing and investing activities. - Interest and dividend income

can either be presented as operating activities, or as investing activities. - Interest expense

can either be presented as operating activities, or as financing activities. - Dividends paid

can either be presented as operating activities, or as financing activities.

FOREIGN CURRENCY CASH FLOWS

Cash flows arising from transactions in a foreign currency are recorded in an entity’s functional currency.

Foreign currency cash flows are translated at the exchange rates at the dates of the cash flows or, when appropriate, using average rates.

The effect of movement in foreign exchange rates is included in the cash flow statement so that the opening and closing balances reconcile.

DISCLOSURES

Note disclosure are required for significant non-cash investing and financing transactions and an explanation of the changes in liabilities arising from financing activities, distinguishing cash flows from non-cash changes. This is often presented as a reconciliation of the financing liabilities.

CONTACTS

| BOAZ DAHARI Moore Israel [email protected] | KRISTEN HAINES Moore Australia [email protected] | TAN KEI HUI Moore Malaysia [email protected] |

| CHRISOF STEUBE Moore Singapore [email protected] | NEES DE VOS Moore DRV [email protected] | TESSA PARK Moore Kingston Smith [email protected] |

| EMILY KY CHAN Moore CPA Limited [email protected] | PAUL CALLAGHAN Moore Oman [email protected] | THEODOSIOS DELYANNIS Moore Greece [email protected] |

| IRINA HUGHES Johnston Carmichael [email protected] | SAHEEL ABDULHAMID Moore JVB LLP [email protected] |

MOORE IFRS in Brief is prepared by Moore Global Network Limited (“Moore Global”) and is intended for general guidance only. The use of this document is no substitute for reading the requirements in the IFRS® Accounting Standards issued by the International Accounting Standards Board (IASB). This document reflects requirements applicable as at the date of publication, any amendments applicable after the date of issuance, to the IFRS® Accounting Standards have not been reflected. Professional advice should be taken before applying the content of this publication to your particular circumstances. While Moore Global endeavors to ensure that the information in this publication is correct, no responsibility for loss to any person acting or refraining from action as a result of using any such information can be accepted Moore Global.